》View SMM Copper Quotes, Data, and Market Analysis

》Click to View Historical Spot Copper Price Trends on SMM

As the conclusion of the "14th Five-Year Plan" approaches, China's power grid investment in 2024 has significantly accelerated. Entering 2025, the State Grid Corporation of China announced a "major" investment plan and optimized its bidding rules. Can this capital injection boost copper wire and cable orders for enterprises? What impact will the rule changes have on companies' bidding success? SMM has compiled feedback from wire and cable enterprises as follows:

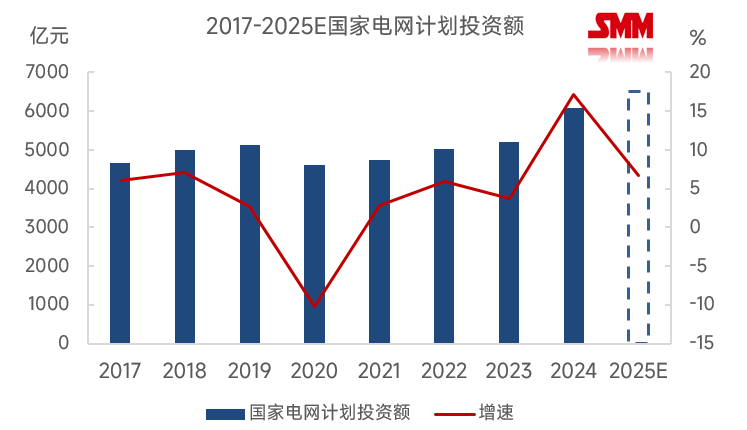

At the beginning of 2025, the State Grid Corporation of China made a major announcement, stating that it will further increase its investment efforts. The annual investment by the State Grid is expected to exceed 650 billion yuan for the first time, while China Southern Power Grid also announced that its fixed asset investment in 2025 will reach 175 billion yuan. Combined, the total investment will exceed 825 billion yuan, setting a new historical record! Overall, power grid investment in 2025 will increase by 47.2 billion yuan compared to 2024, up over 6% YoY.

Data Source: National Energy Administration, State Grid Corporation of China

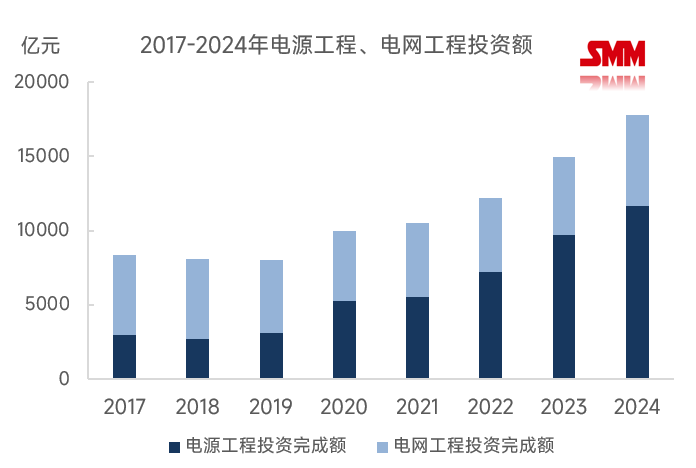

The significant increase in power grid investment reflects the country's efforts to address the issue of new energy electricity consumption. Since 2020, China's power supply investment growth rate has been significantly higher than that of power grid investment, and the proportion of power supply investment has also been notably higher. Clearly, there is an imbalance between power supply and power grid investments, with power grid investment lagging behind.

To match the rapid development of power supply construction, China must accelerate the pace of power grid construction. However, in recent years, to address the electricity consumption issues of large wind and solar power bases, ultra-high voltage (UHV) transmission networks have become the focus of power grid construction. UHV primarily uses steel-core aluminum stranded wires, which will significantly boost aluminum wire and cable demand, while the impact on copper wire and cable orders will be relatively small.

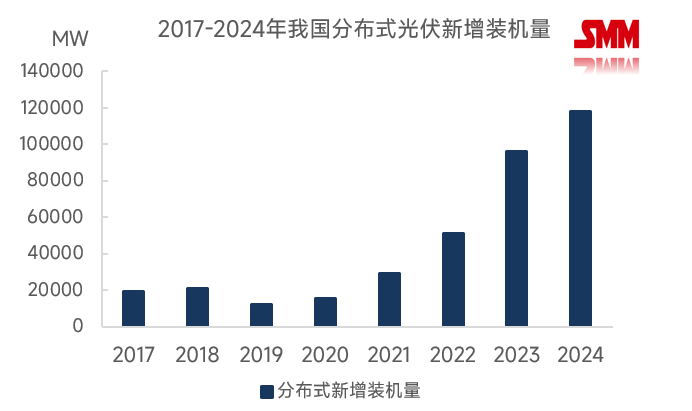

The growth of copper wire and cable orders mainly depends on the distribution network segment. According to publicly available data compiled by SMM, the proportion of distribution network investment in 2024 is at a relatively low level in recent years, indicating that UHV investment has crowded out distribution network construction. However, due to the overall increase in total investment, the total amount of distribution network investment is expected to show a growth trend, though its proportion remains around 50%, with no significant increase. In recent years, the rapid growth of distributed energy in China has also been notable. To address the electricity consumption of distributed energy and the demand for charging pile integration, SMM expects the proportion of distribution network investment in 2025 to increase, which will also drive demand for copper wire and cable. However, it is worth noting that high copper prices may accelerate the industry's shift toward "aluminum as a substitute for copper," limiting the growth of copper wire and cable orders.

According to SMM, based on this year's bidding and award results from the State Grid and China Southern Power Grid, some copper wire and cable enterprises have reported a noticeable increase in both bidding volumes and awarded contracts. March and September are the busiest periods in terms of bidding frequency. Although most enterprises have not felt a significant difference, SMM believes this is a result of intensified industry competition, as the "pie" is indeed getting larger.

Additionally, the State Grid has adjusted its procurement rules this year: for seven categories of materials, secondary regional joint procurement will be organized, and individual units will no longer conduct secondary procurement independently, effective January 10, 2025. Some wire and cable enterprises have expressed concerns about regional concentration of orders under this policy, fearing that their original bidding advantages may be weakened, potentially affecting their awarded contract volumes. However, this is not expected to impact the overall copper consumption in the market.

Overall, 2025 marks the conclusion of the "14th Five-Year Plan," and the investment plans announced by the State Grid and China Southern Power Grid have provided a strong boost to the market. Power sector orders are essentially guaranteed. SMM expects China's copper consumption in the power sector to grow 2.59% YoY to 7.53 million mt in 2025. However, enterprises will need time to adapt to changes in market rules. With multiple factors influencing the market, copper wire and cable enterprises will face increased challenges in securing orders this year. For these enterprises, 2025 will remain a year of both challenges and opportunities.